A look at the current state of the crypto brokerage industry.

Teams from Binance Broker and Binance Research

15 September 2020

- Financial markets have seen brokers evolve since the 1970s to satisfy the ever-increasing needs of market participants.

- Prime brokers provide liquidity, trade execution, custody, clearing, settlement, capital introduction, trading on margin and derivatives services, and more in traditional markets, effectively acting as a one-stop-shop for institutional clients.

- Many brokers, on the other hand, rely on services supplied by “core brokers” (i.e., brokers of brokers), allowing them to focus on value-added services such as marketing, client acquisition strategy, dedicated customer service, and liquidity and settlement services.

- In the developing crypto business, two types of brokers have emerged: prime brokers and broker service providers (sometimes known as “core brokers”). Following initial attempts to offer CFD crypto trading to clients, fintech and FX brokers have shown a stronger interest to become more involved in the industry.

- Despite the fact that the cryptocurrency market often gives faster access to trading venues than traditional markets, institutional investors continue to require trading, compliance, and liquidity services from prime brokers.

- Traditional brokers have not offered spot crypto services due to regulatory restrictions (only derivatives and other instruments). As a result, crypto exchanges have become the epicenter of the nascent crypto brokerage sector.

- As a result, prominent crypto exchanges have developed prime brokerage services to provide custody, block trading, aggregation trading, and other services to institutional investors.

- Meanwhile, crypto broker service providers have empowered brokers to offer services to institutional participants from both crypto and traditional brokerage environments, promoting the industry’s lateral expansion through non-crypto companies offering dedicated crypto trading to their users, which is expected to lower entry barriers even further.

- Brokers have become a critical component of the services given to institutional clients as institutional trading has grown more generally accepted in the crypto industry. The crypto brokerage sector has experienced tremendous expansion and development, adapting to the specific needs of significant market participants on a regular basis.

- This paper uses case studies to examine the crypto brokerage market and compare it to the traditional financial broker industry before examining some of the current trends in the crypto brokerage industry.

1. A general overview of the brokerage business

1.1 What is the structure of the traditional brokerage industry?

The traditional financial market has a fine-grained labor division, with brokers providing a variety of trading services to investors, which helps to drive market expansion. There are currently over 3,600 security brokers in the United States, with market revenue of $300 billion expected by the end of 2023.

In the traditional equities brokerage market, there are three main players: exchanges, investors (including institutional and retail), and security brokers.

A stock exchange is a place where people may purchase and sell stocks. Only eligible members have access to trade on exchange venues in traditional equities markets. Its primary roles are as follows:

- Providing trading access and infrastructure to investors.

- Organizing and supervising trade activity, as well as order management.

Investors (both institutional and individual) in traditional markets frequently face the following limitations:

- For regulatory reasons, most investors are unable to trade directly on exchanges.

- They place a high emphasis on value-added services.

Security brokers serve as a link between investors and exchanges. Their primary responsibilities are as follows:

- When investors entrust you with the purchase and sale of securities, you might earn commissions.

- Provide consultancy services to investors, such as investment advice and asset management.

- Financial instruments including leveraged products and securities lending are available.

There are a variety of brokers to meet the diverse needs of different financial market participants. Brokers can be classified in a variety of ways, including the type of trading they do, the business strategy they use, and the partnership model they use. Large banks have begun to offer a variety of brokerage services, each with its own set of segmentation that may be adjusted to their own business lines.

(1) Divided by the trading object

- Customers who want to make financial investments should seek the advice of security brokers. Securities brokers make purchases and sales of stocks, bonds, and other securities on behalf of their clients.

- Foreign exchange (or Forex) brokers are companies that provide traders with a platform via which they can purchase and sell foreign currencies.

- Futures brokers are traders that specialize in dealing with futures contracts for commodities.

- Crypto brokers: These are companies (or individuals) that function as middlemen between cryptocurrency markets, making it easier to buy and sell cryptocurrencies.

(2) Business models are divided into two categories.

- Discount brokers charge lower commissions for trading execution and typically do not offer any advisory services. Robinhood and E-trade are two examples.

- Full-service brokers charge higher fees since they focus more on offering value-added services (such as wealth management). Merrill Lynch, Morgan Stanley, and UBS are well-known names in the traditional financial industry.

(3) Based on the type of collaboration.

- Introducing brokers connects clients with brokers who earn commissions by executing trades and settlements. Such brokers are more likely to focus on marketing.

- Non-disclosed brokers have wholly-owned brands and products that are built on larger brokers’ underlying infrastructures. Non-disclosed brokers, in contrast to introducing brokers, typically offer a full range of services to their clients.

Brokers come in a variety of shapes and sizes, but they always aim to connect exchanges and users. The integration of business-side resources to create business/client-side interactions or the expanding number of direct business/client-side relationships is a never-ending battle for brokers.

1.2 The instance of prime brokers, a typical traditional financial broker

The term “prime brokerage” was originally used in the late 1970s. Trading, settlement, and custody were previously handled by different entities. Institutional customers frequently engage many security vendors to collaborate on these tasks. As a result, fund managers were burdened by the massive volume of trade data.

The primary purpose for the establishment of the prime broker sector was to centralize operations such as trading, settlement, and custody. Since then, prime brokerage firms have added a variety of services to give institutional clients a one-stop financial shop.

Prime brokerage firms provide services to their clients in traditional financial markets, such as:

- Trading, custody, settlement, valuation, risk management, and operations are all aspects of the business.

- Portfolio reports and business reports are two different types of reports.

- Derivatives such as margin and stock buybacks are designed and implemented.

- Margin trading is when you trade on a small amount of money.

- Controlling the flow of money.

- Personalized technical assistance.

- Other services that provide value (including capital introduction, risk management consulting, and more).

As a result, prime brokers mostly profit from:

- Commissions on trading.

- Fees for custody and settlement.

- Margin trading and other leveraged trading spreads are two types of leveraged trading spreads.

- Fees associated with asset management and consulting.

Prime brokers are used by funds, particularly hedge funds. Although settlement services account for a minor portion of securities brokers’ revenue, a significant portion of prime brokers’ revenue comes from offering settlement-based services to hedge funds, such as margin trading and other services.

Companies like Interactive Brokers, in addition to providing brokerage services, also provide underlying channel services for institutions and retail users to other brokers.

The diagram below shows an example of a tiered structure of brokers and broker services.

One of the major online security brokers in the United States is “Interactive Brokers.” It provides underlying channel services for online securities, operating as a one-stop-shop for fully disclosed and omnibus brokers, offering trading, settlement, and other services.

An omnibus broker, “Tiger Brokers,” caters to Chinese clients seeking exposure to foreign securities such as US shares. Tiger Brokers receives trading, settlement, and other underlying services for US stock trading from Interactive Brokers. As a result, Tiger

Brokers concentrate on user acquisition through aggressive marketing and committed customer service.

“Snowball Securities” is a fully-disclosed equities broker designed to give investors access to worldwide securities listed on major stock exchanges (such as the Hong Kong Stock Exchange (SEHK), the New York Stock Exchange (NYSE), and the NASDAQ).

1.3 What is a crypto brokerage, and how does it work?

1.3.1 Cryptocurrency brokerage requirements

The situation of the crypto brokerage market is fast evolving, owing to the present rush of forex brokers and fintech firms into the crypto world. The crypto business, which was once dominated by a retail presence, has been rapidly growing in recent years.

Crypto brokerage business pioneers have steadily established an underlying architecture that is increasingly resembling that of the traditional financial sector.

Forex brokers initially joined the industry by offering CFD products, while Fintech firms entered the market by establishing fiat channels.

The ecosystem has organically evolved into two key parts in the formation of the crypto brokerage space:

Tagomi, for example, is a prime broker providing pooled liquidity for institutional clients. They cater to institutional and sophisticated investors.

The ecosystem has organically evolved into two key parts in the formation of the crypto brokerage space:

- Tagomi, for example, is a prime broker providing pooled liquidity for institutional clients. They cater to institutional and sophisticated investors.

- Large exchanges, like Binance and Paxos, are assuming the role of brokers and providing underlying liquidity to other brokers (through itBit). They try to connect liquidity for outside market participants, effectively expanding their scope and eventually serving a wider user base.

Because market participants’ criteria are limited compared to traditional financial markets, the crypto industry does not have the idea of “trading seats,” as it does in the traditional financial sector.

Brokers, on the other hand, are still relevant in a variety of ways:

Due to the high entrance barriers at larger venues, brokers are conducive to integrating market resources and play a significant role for small and medium businesses in the industry.

With changes in market demand, prominent players’ resource integration capabilities are gradually improving.

Lower costs, fewer operational risks, and the ability to specialize in a small subset of operations are just a few of the advantages.

(1) Cost savings

- Internal and external market makers: market participants do not have to pay for internal and external market makers if they use a brokerage service.

- Develop matching/trading engines: Participants can save money by not having to build matching/trading engines, which take a lot of time.

- Infrastructure for wallet systems: A sophisticated wallet system for crypto assets is not necessary to be built and maintained.

(2) Lowering of operational hazards

- Trading underlying system: decrease the underlying trading system’s operational risks.

- Risk control system: It decreases technical risk from the standpoint of end-users by utilizing mature and comprehensive risk control systems from brokerage service providers.

- Product design: Market participants frequently rely on designed products from third-party providers to reduce business risk.

(3) An increase in the number of innovative and high-value-added services

- Value-added services: Crypto brokers could offer clients value-added services such as trading methods, trading bots, and asset management, among other things.

- Product innovation: Because heavy technical components are handled by a third party, brokers can devote more time to product development, expansion of new channels, and customer acquisition. Brokers, for example, are not required to regularly monitor network upgrades (e.g., soft forks, etc.).

Due to legal restrictions, traditional financial exchanges were unable to launch a brokerage firm. As a result, bitcoin exchanges have expanded by establishing specialized brokerage services.

The graph below demonstrates that traditional exchanges are already doing a lot of business as broker service providers and that more and more exchanges are moving into prime broker territory.

Institutional investors’ need for trading and financial services is the driving force behind crypto prime brokerages. Some cryptocurrency exchanges, wallets, and trading platforms have started offering prime brokerage services. For example, Coinbase provides prime brokerage services that begin with custody, whereas Huobi and Bequant provide prime brokerage services that include OTC block trading. A prime broker’s primary goal is to service institutional investors.

- Liquidity, financial instruments (such as margin, loan, and so on), settlement, and compliance are all necessities for clients.

- Custody, trade, and financial services are examples of product services.

- Professional trading instruments such as block trading. For investors to benefit from optimal liquidity and improved trading execution, brokers pool liquidity from various exchanges. Coinbase and Huobi are two examples.

- Institutional investors receive financial services such as margin, lending, and other financial services.

While prime brokers target institutional investors, broker service providers, through liquidity services offered to intermediary businesses, ultimately target individual investors.

As previously said, crypto brokers can be divided into two categories:

- Crypto prime brokers: firms like Coinbase and Paxos specialize in offering compliant cryptocurrency trading services to fintech firms, banks, and other financial institutions.

- Broker service providers, such as Binance Brokerage, provide crypto services to other brokers serving individual investors, such as liquidity provision and custodianship.

This terminology was established for the purpose of this research to separate participants in the crypto brokerage sector.

Because crypto markets are still in their infancy, this breakdown aids in the classification of those brokers that only give services to institutional clients in the crypto business, as opposed to those who provide services to other brokers, catering to retail traders. Changes in the industry and business are unavoidable, making this analysis less relevant.

2. Crypto-brokerage industry case studies

2.1 Coinbase (prime broker Plus broker service provider) is the second option.

Both prime broker services and broker service solutions are available from Coinbase.

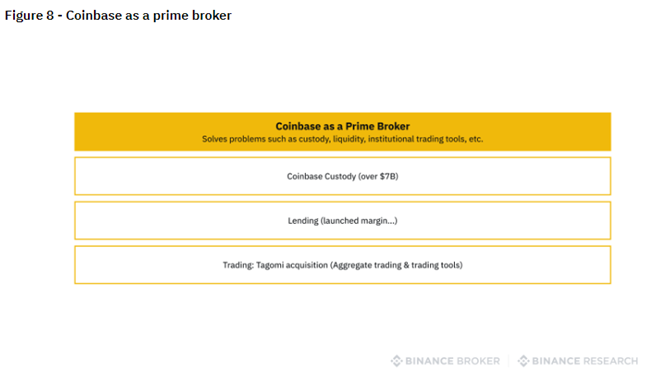

2.1.1 Coinbase as a prime broker (Tagomi)

Tagomi is a prime broker that offers institutional clients a wide range of services, including aggregated trading (from Coinbase, Bittrex, Kraken, Gemini, Bitstamp, Binance, and other significant liquidity venues), custody, margin, lending, and staking. It was bought by Coinbase in May 2020.

- Institutional customers are the intended clients (e.g., hedge funds, private equity funds, crypto funds, quant funds).

- BitLicense and insured custodianship services are two of the company’s strongest assets.

- Services:

- Coinbase Custody is a custodial service.

- Margin trading (on Coinbase Pro, for example) and other forms of lending

- Trading: professional trading instruments and aggregated trading.

- Paradigm, Pantera, Bitwise, and Multicoin Capital are just a few examples of clientele.

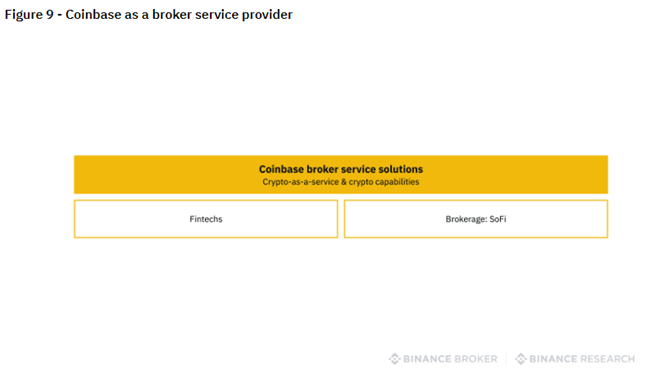

2.1.2 As a broker service provider, Coinbase

Since 2019, Coinbase has given broker service solutions.

- Fintech firms, brokers, and banks are all potential clients.

- BitLicense and insured custodianship services are two of the company’s strengths.

- Broker service solutions are offered as a service.

- Clients as an example:

- SoFi is a personal finance company based in the United States that serves 1 million customers with loans, mortgages, stocks, and cryptocurrency investments. Since September 2019, SoFi has partnered with Coinbase to offer crypto trading. It was granted a BitLicense in December of this year.

2.2 Paxos’ role as a broker service provider

Paxos Brokerage, which began operations in July 2020, seeks to deliver a set of API-based, compliance crypto trading and custody solutions to brokers. Paxos’ own exchange, itBit, provides liquidity (with a base rate of 0.35 percent).

- Payment companies, wealth management firms, banks, and other fintech firms are all potential clients.

- BitLicense, API connectivity, and custody services are among the company’s advantages.

- Brokerage services for institutional clients are provided.

- Clients include the following:

- Revolut is a fintech firm based in London with 12 million customers and a $5 billion USD valuation. Payments, FX, stock trading, digital currency trading, and other services are currently available through Revolut.

- PayPal is a service that allows you to (unofficially public).

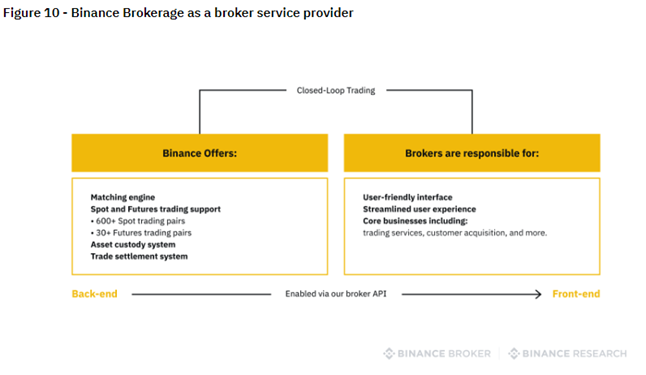

2.3 Binance as a broker service provider

Binance Brokerage aspires to be the crypto industry’s liquidity provider.

- Exchanges, wallets, trading bots, market data platforms, asset management systems, and others are examples of clients.

- Strengths:

- Exchange operations provide a lot of liquidity.

- Derivatives, loans, and margins are just some of the trading instruments available.

- Staking and on-chain services are examples of crypto-native services.

- Services:

- Spot trading, futures trading, and fiat trading are the three main types of trading.

- Lending, financial management, mining, and payments are examples of upstream/downstream interaction.

- A wide range of assets is supported for spot and futures trading.

- There are 600+ spot trading pairings, with several unique trading pairs and a huge number of altcoins available.

- With settlement in both base and quotation assets, there are more than 30 futures trading pairs, including unique altcoin derivatives assets.

- Asset custody system: Asset custody is handled at the exchange service level, allowing Binance.com to provide services for any of the supported assets.

- Trade settlement system: deals are settled at the exchange level, with funds being transferred straight to the wallet.

Binance’s broker API allows clients to integrate both back-end and front-end infrastructure.

3. What is the crypto brokerage industry’s outlook?

The gap between the traditional financial market and the crypto market will continue to close as the crypto business develops.

A virtuous cycle of expansion began with a rising base of retail and institutional customers, an expanding market, and the introduction of increasingly specialized functions.

Brokers have evolved into “supernodes,” connecting individuals seeking to trade a wide range of assets.

In this regard, we’ve discovered three major trends:

- Traditional brokers are now providing cryptocurrency services.

- Existing crypto prime broker activity will be diversified.

- Broker service providers must comply with several regulations.

Trend 1 – Traditional brokers offering crypto services

- As they move toward a full-service brokerage model, top prime brokers are expected to transfer their focus to wealth management.

- Traditional financial institutions have entered the cryptocurrency and digital asset markets by providing spot trading services to their current customer base (mostly non-crypto users).

- Meanwhile, the shift from bargain broker to full-service financial services provider may attract customers through technology and product innovation, resulting in more customer segmentation.

Trend 2 – Diversification of crypto prime broker activities

Companies that provide prime brokerage services have been looking toward high-value-added services.

- Coinbase (for its prime broker activities), BitGo, and several competitors began dabbling in prime brokerage in 2020, although the practice is still in its early stages.

- Prime brokers have built a diversified revenue structure in the traditional financial industry as a result of a broader variety of profit-generating business lines. Crypto prime brokers, on the other hand, have an extremely concentrated income structure (highly dependent on a single asset class). Nonetheless, as the gaps between the traditional and crypto markets narrow, they are projected to diversify in the future.

- To address the demand of institutional traders and other financial institutions, cryptocurrency prime brokers have begun to offer services such as custody (e.g., mutual funds, hedge funds).

Trend 3 – Compliance requirements for broker service providers

While more fintech companies, traditional brokers, and other banking institutions are looking to offer crypto services to their customers, compliance is still a major concern.

- Cryptocurrencies and other digital assets have piqued the interest of fintech firms. Fintech companies may be able to help the crypto industry expand its horizons once regulatory constraints are adequately defined and addressed.

- Brokers’ crypto CFD products (like Robinhood and eToro) are suboptimal because of slippage, excessive spreads, and pricing complexity while being compliant in various countries.

- Brokerage service providers (for example, Binance Brokerage) are attempting to create a more compliant environment for clients by leveraging liquidity from crypto exchanges to partner brokers and clients in both traditional and crypto markets, in order to promote the growth of the crypto industry as a whole.