ow, will the Russia-Ukraine crisis impact crypto markets?

ShivX Research (Maharshi)

April 2022

- Crypto has been at the forefront of conversations surrounding the Russia-Ukraine crisis;

- exchange data for Russian and Ukrainian users reveal increased activity in the previous few weeks as the local population reacts to the realities of sanctions and military conflict. Despite this, the numbers are small, indicating that both countries are still in the early stages of crypto adoption.

- Crypto cannot be utilized by Russians to escape sanctions in any meaningful way, both in terms of liquidity and anonymity, as evidenced by data.

- The directional connection between crypto and stocks, as well as within crypto markets, has recently reached new highs, but crypto continues to outperform. The disparity between commodity markets and equities suggests a re-calibration of correlation assumptions, which supports the case for crypto outperformance.

- While the digital gold theory appeared to be faltering in the early days of the dispute, crypto has rebounded dramatically in recent weeks, while gold prices have remained stable. The effects of the crisis on already-high global inflation will almost certainly reinforce the Bitcoin inflation hedging theory in the future.

- The combination of monetary weaponization via reserve asset freeze, recent Canadian government moves, and a shift in the globalization narrative supports a bullish view of crypto in the longer term, with the crisis pushing broad adoption and hastening the transition to a more digital world.

The conflict between Russia and Ukraine is the first significant armed European conflict in decades. The crisis is still evolving, and there is a thick fog of war in both the media and on the ground. With the widespread use of international sanctions against Russia and Ukraine’s digitally-minded people, crypto has been at the forefront of the crisis’s talks. On the one hand, Ukraine has received more than $70 million in cryptocurrency donations, while on the other, regulators are debating how Russians can use it to circumvent sanctions, with calls for big exchanges to restrict local users. In many ways, this may be considered the first-ever crypto war.

In this analysis, we examine what has occurred thus far, how it relates to prior market-moving events, how the scenario has affected crypto in the near term, and what we estimate the long-term effects to be.

What has happened so far?

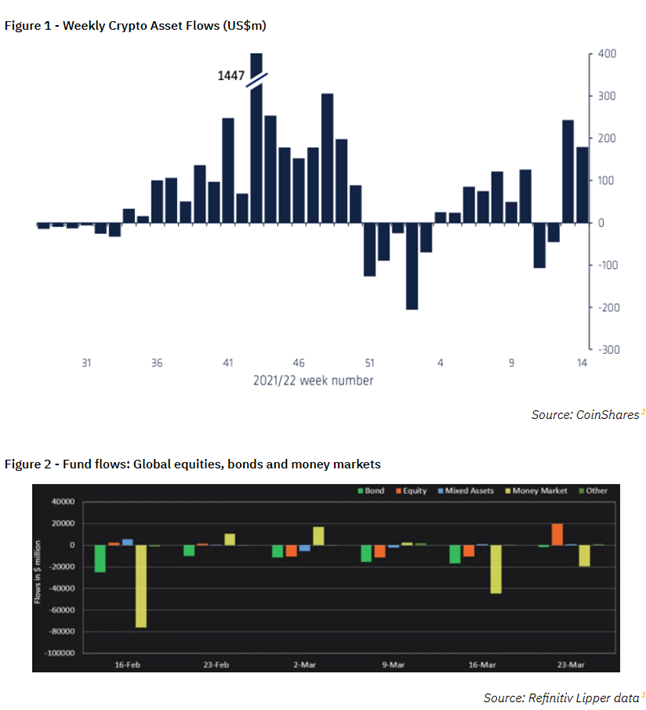

To begin, we examine how the situation has played out so far in terms of capital flows. According to a preliminary examination of trading flows, weekly crypto-asset flows showed a significant increase in inflows in the weeks leading up to the crisis’s onset on February 24th. When compared to global market movements, we can see a significant difference emerge, with equities experiencing net outflows in the same periods as crypto assets had inflows. Perhaps a forewarning sign that some market players are moving away from stocks and toward riskier crypto assets. The fact that they were suffering outflows previous to the crisis, while stocks were receiving inflows, and that this pattern reversed after the crisis, as illustrated below, indicates that crypto’s role as a hedge to traditional market assets is being recognized and used.

While we do see a slight rise in net fiat inflows and activity when we look at specific countries’ flows using data from major exchanges for Russian and Ukrainian customers, the numbers are not exceptionally significant. So, what does this mean? This can be thought to be Russians selling rubles in exchange for cryptocurrency assets in order to preserve their wealth and respond to capital limitations imposed by the Bank of Russia. Let’s not forget that since the beginning of the crisis, the ruble has lost almost 11% of its value against the US dollar, and at one time was down 96 percent as incoming sanctions news combined to create a near-‘rug pull’ of the currency. Crypto assets may have been, and continue to be, the only realistic means for certain people in the country to retain their fortune. Ukrainians are likewise concerned about the preservation of wealth, though not from the standpoint of currency depreciation, but rather from the perspective of individuals who may be forced to flee their homes without having time to liquidate their holdings. Aside from that, UAH pairings on crypto exchanges will reflect some liquidation of the country’s claimed $70 million in cryptocurrency gifts. The low levels of activity suggest that crypto adoption is still in its early stages in both countries and that it is far from the preferred method of trading with one another – at least at this early juncture in the crisis.

Another factor to examine is the story of Russians’ potential use of crypto to circumvent sanctions. To begin, we might discount the concept that such evasion could occur on a broad scale. Understanding that Russia has lost access to at least half, if not all, of its $630 billion in central bank reserves is an easy way to illustrate this. With all crypto’s present market capitalization of only $2.1 trillion, it’s evident that the crypto markets can’t be utilized to shift or replace any significant portion of those frozen reserves. Any large-scale avoidance on a national scale is thus ruled out.

Individual actors might theoretically utilize crypto to move funds and possibly escape personal punishments on a more detailed level. However, given that blockchains are by their very nature traceable, we may look at a number of signs to see if this is the case. To begin, we can consider the fact that crypto wallets can give some anonymity, especially when used in conjunction with mixer protocols like Tornado cash. To that end, we’d like to point you to a recent report4 from crypto data company Chanalysis, which has been keeping a close eye on known Russian whale wallets and activity on high-risk services like Tornado cash, as well as smaller, riskier exchanges like Garantex and Bitzlato. For all of the channels they monitor, their report reveals no significant spikes in inflows, outflows, or odd activity. This is in accordance with testimony given to the United States Senate by co-founder Jonathan Levin and a number of other experts during a recent hearing5 on the use of digital assets in illegal finance.

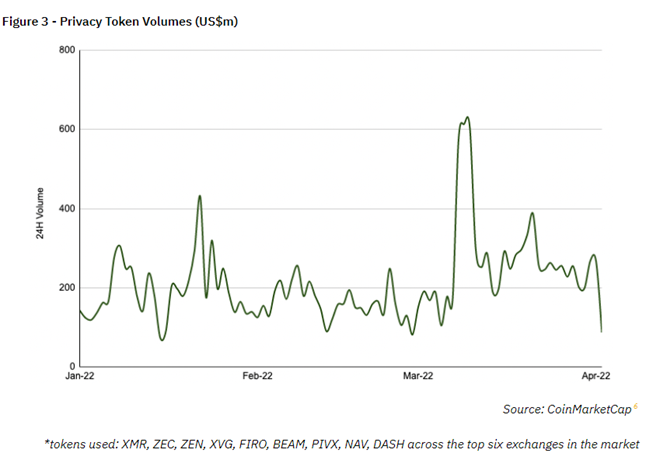

We might also explore a quick examination of specific privacy coins, which individuals may aim to utilize to conceal transactions. However, as you can see in the graph below, there has been no discernible increase in transaction levels of the top privacy coins, despite a significant increase in Russian activity in general (the slight spike in early March in privacy tokens was largely attributed to a then-upcoming

a crypto executive order from President Biden). Furthermore, on decentralized platforms, the liquidity required to facilitate any material evasion of sanctions is simply not there. When you consider that any fiat off-ramps that only exist through centralized intermediaries will be unable to be utilized without being traced, it’s evident that the Russian government and people are unlikely to adopt crypto to dodge sanctions.

How does this compare to previous periods of market turbulence?

The start of the Covid-19 pandemic in early 2020 is a recent case study for how global markets have reacted to this news. We observed a 44 percent drop in overall crypto market capitalization in ten days (the biggest buying opportunity in recent years), followed by a fast rebound and rapid escalation, breaking through the previous local peak within two months. Using the MSCI World Index7 as a proxy for global equities, there was a 32 percent loss in equity markets from January to March. It took over five months to return to the prior level, after which it spent the entire year of 2021 in an upward trend. When compared to the current market downturn, crypto has dropped 24% from its February highs, while global stocks have been down 10%. However, the crypto markets have now made a strong comeback, rebounding within a month, while global equities have remained unsettled. More specifically, after the onset of the crisis, Bitcoin fell around 11%, while the MSCI World Index fell 5%. Since then, Bitcoin has recovered all losses and is now trading at approximately $47,000, although the MSCI World Index is up less than 8%.

When we examine these trends from a correlation standpoint, we can see that crypto appears to trade in the same direction as a risk asset and responds to stock swings. The 90-day correlation between Bitcoin and the S& P500 was recently reported8 to have reached its greatest level since October 2020. While the 90-day correlation shows this, shorter-term indicators show a totally different picture, as crypto markets bounce back and outperform at a much faster rate than regular equities markets, as one would expect. Another form of correlation to consider is the one between Bitcoin and Ether, as well as the overall crypto market. The 90–day correlation for both of these metrics is approaching all-time highs, similar to the bear markets of 2018 and 2019 and the Covid-19 sell-off of 2020, according to the data. The noteworthy aspect is that in prior cycles, the high crypto correlation was triggered by rapid selloffs, whereas this era of high correlation has corresponded with a more steady growth pattern, implying that diversifying Bitcoin holdings through altcoin exposure is not an easy task. Furthermore, the fact that both of these connections tend to peak near times of market stress might be linked to a decreased desire to rotate into altcoins and, as a result, a risk-averse market climate.

The commodity market, which has experienced a divergence from equities, in what is extremely different from last year, has already seen the recalibration of the linkages that market players are expecting. As shown in the graph below, both markets grew in 2021, albeit at slightly different rates. However, as tensions in Eastern Europe escalated, commodities skyrocketed in price, in stark contrast to global equities, which plummeted. While the motivations for this trend are mostly supply-side, given both countries’ energy and agricultural production capacities, the concept of altering correlations lends itself nicely to creating a thesis for crypto outperformance in the medium run. Given all that a permissionless and trustless system can provide in comparison to the clearly censorable and permissioned fiat system many of us are witnessing up close for the first time, there is a compelling case for crypto markets to do the same, similar to how commodity markets are reacting to this shift in the globalization narrative.

What does this mean in the short term?

We might explore what this recent performance means for the original Bitcoin as a digital gold theory in order to address the immediate repercussions. As previously said, as the conflict began to take shape, Bitcoin, like most other risk assets, saw its value plummet. Gold, on the other hand, increased by 3% and reached a local high of $2,044/oz, up 8% from the start of the crisis. If you take this at face value, it appears that some very outspoken gold maxis have finally been vindicated, but what happened after the first shock? As can be seen, Bitcoin has recovered steadily and is now around 35% higher than its local low, whilst gold looks to have adjusted lower and is currently trading sideways. We could argue that the subsequent price movement reflects Bitcoin’s strengthened status as digital gold, but it’s probably better to consider, whether or not it’s digital gold, Bitcoin, and crypto-assets are part of the safe-haven discourse. Simply because crypto assets are included in the category of hard assets, and the distinction between them and fiat currency is becoming more apparent, Bitcoin’s status as digital gold is justified. As the year progresses and more data becomes available, it’s possible that Bitcoin and cryptocurrency may continue to surpass actual gold, putting an end to the debate once and for all.

Another narrative worth considering is Bitcoin’s usefulness as an inflation hedge. Inflation has been on the rise in most industrialized countries for some months, while Bitcoin and the broader crypto markets suffered a gloomy first quarter, at least in terms of price action. Is this to mean that, in the absence of genuine inflation, Bitcoin isn’t the inflation hedge that everyone has been talking about? Both yes and no. Price swings in the near term may not always correlate to what could be called effective hedging. However, we believe that you must prolong the time horizon in order to adequately assess Bitcoin’s and crypto’s function in general. When it comes to US monetary policy, many people, including Fed employees, believe that the Fed, for lack of a better term, fell asleep at the wheel. For months before the onset of the Russia-Ukraine crisis, the US CPI had been smashing multi-decade records, with the famed ‘transitory’ inflation story running rampant, attributing the pent-up demand from two years of lockdowns as the impetus behind inflation. We saw the crisis emerge and the dramatic spike in energy and commodity prices only a few months after Fed Chair Jerome Powell formally rejected the word ‘transitory.’ This supply-driven inflation has yet to be officially reflected in the inflation readings of most industrialized countries, and it is this that leads us to believe that the Fed, as many of its peers, may be too late in limiting inflation. When this new source of price movement begins to show up in CPI readings, the Fed will be even more frantic, with stagflation appearing to be the most likely consequence. In this context, Bitcoin’s role as an inflation hedge will be put to the test, and we believe it will be confirmed.

What about the medium term?

The weaponization of the monetary system that we witnessed across the globe when countries came together to freeze Russia’s central bank reserves would undoubtedly have far-reaching implications for the global financial system as a whole. The central bank reserves of a country are no longer as reliable as they once were, necessitating a re-pricing of all foreign reserve assets. In a financial sense, the discount rate at which we have been pricing sovereign savings has risen all across the world, particularly for countries that may not be favorable to Nato, the United States, or any other group, whether local or international. Who will be the next country’s foreign reserves to be targeted?

Looking 7,000 kilometers west of Moscow, we find another episode that may have been overlooked by the happenings in Eastern Europe but could be even more important in propelling crypto usage ahead. The Canadian government used the Emergency Act in February to order traditional financial institutions to freeze the accounts of people who were protesting the Covid-19 mandate truck driver strike in Ottawa. Apart from the fact that the government used the monetary system as a weapon, it also included people who just indirectly supported the protest through their donations. Although the embargo was lifted after a week, the acts set a hazardous precedent. Those who say that freezing Russian central bank assets is an act carried out in the heat of conflict and not something that would be expected in more ‘calm times’ will find that this is simply not the case.

Another thing to think about is the globalization narrative shift and how it connects to this. Over the last few decades, countries have discovered that there are significant benefits to be obtained by going outside, whether for cheaper labor or lower regulatory requirements; the gains were obvious, while the hazards were neglected. Interdependence became the norm as countries and businesses began to globalize. Then came Covid-19, and the first great understanding that our dependency has reached a previously unseen level, and that even a minor disruption in our supply lines can quickly devolve into anarchy. The Russia-Ukraine crisis has exacerbated this narrative shift, not least because, although the US continues to impose sanctions, Europe has been unable to sanction Russia’s most crucial resource: energy. The fact that continental Europe is unduly reliant on Russian energy is a sobering reminder that globalization has its drawbacks and that we are increasingly living in a world where good relations with other countries are critical to our national infrastructure. The acknowledgment of our interdependencies has already begun to force governments and enterprises to reassess their operations, which will most certainly result in an increase in onshoring or nearshoring. Perhaps the next major narrative will be a change toward finding the safest, rather than the cheapest or easiest, sources for our economic demands. According to Howard Marks, the pendulum is clearly swinging away from globalization.

By combining these concepts, we should have a better notion of what to expect from crypto in the medium future. The preceding examples of monetary weaponization are clearly dangerous precedents that will surely drive the use case for governments, businesses, and individuals to possess non-fiat instruments. As more countries seek to develop wealth in assets that cannot be frozen or restricted, the shift away from globalization and toward a more localized economy adds to this use case. Crypto may emerge as the clear winner, owing to its function as a payment system that is subject to far less meddling than the current financial system. In addition, if the next iteration of the global age is marked by greater distrust than the previous few decades, a trustless and permissionless system based on blockchain technology will be unavoidable.

Conclusion

The Russia-Ukraine conflict, or possibly the first crypto war, has forever altered the landscape. The capacity to interact with a global network of citizens and generate funds in the midst of a military crisis is a quantum leap beyond what was previously thought conceivable. The weaponization of our current monetary system significantly amplifies the importance and reach of non-fiat, crypto assets, accelerating the transition to a digital, crypto-centric future. Markets appear to be rebounding strongly, with Bitcoin trading nicely and the whole crypto market worth up 24% in March and continuing to rise. What remains to be seen is how much of the $13 trillion in global foreign exchange reserves10 enters the $2 trillion crypto market.